Decentralized Loans on Ethereum

Decentralized Loans on Ethereum

How Aave is democratizing loans using crypto

Welcome back! Today we're taking a look at Aave, the largest decentralized lending platform. Aave is huge. With $15 billion in value deposited on the platform, Aave is crypto's biggest protocol by Total Value Locked (TVL).

If you've been reading along, you'll know that crypto is so much more than a digital currency. It's the future of the internet, a way to build decentralized products and services that have real use cases and generate real cash flows. Aave is a great example.

Aave's History

Stani Kulechov, a lawyer by education, founded Aave in 2017 as a peer to peer lending protocol built on the Ethereum network. Prior to University in Finland, Stani dabbled in building some fintech products.

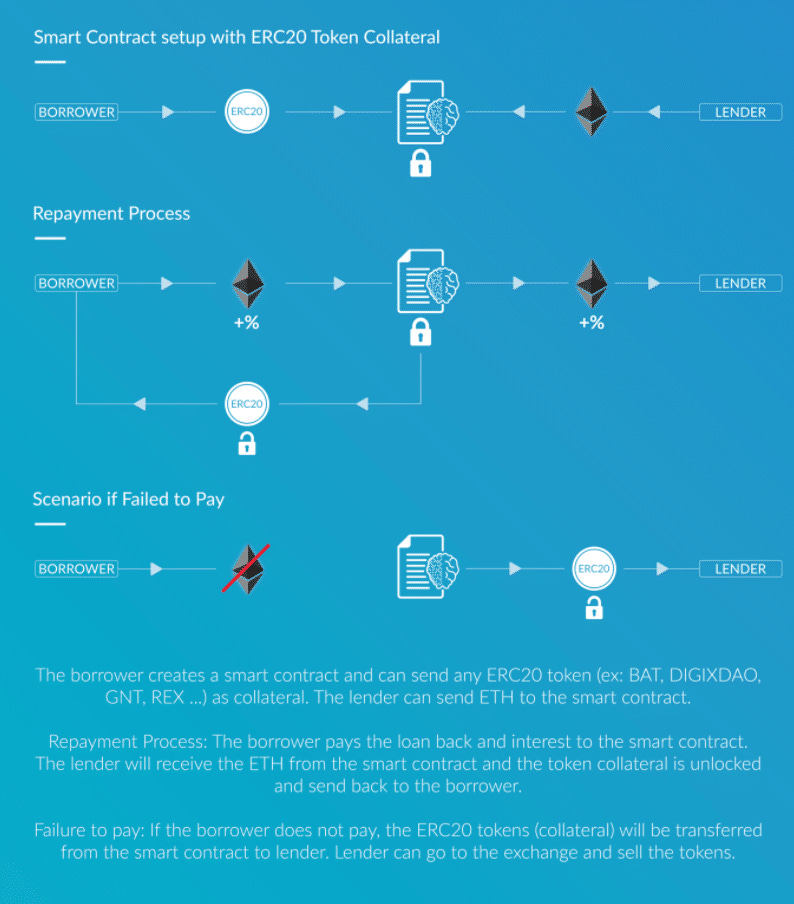

Back in 2017, Aave was actually called ETHLend. ETHLend used a peer to peer model to facilitate borrowing and lending assets on top of Ethereum. A borrower and a lender could agree on important terms of the loan independently of banks, loan officers, or bureaucracies. (Notice how cutting out middlemen is a recurring theme in crypto). The two sides agreed to the interest rate, the level of collateral required, and how long the loan would last.

After agreeing on terms, borrowers and lenders were able to create secure contracts that protected each party. Lenders deposited the loan amount to the smart contract while borrowers posted collateral (an ERC-20 token) to the smart contract. Neither side could unlock the collateral until the loan was either 1) paid back or 2) defaulted on.

In the first scenario, the borrower paid back the loan with interest. Once the smart contract received that payment, the borrower received their collateral back and the lender was paid the loan amount plus any accrued interest.

What happened if the borrower defaulted on their loan? If the borrower's collateral dropped below the agreed amount, the smart contract would distribute that collateral to the lender to protect the lender from losing their investment.

ETHLend was among the first protocols to democratize lending; anyone was able to use the platform without any know your customer (KYC) checks, bank accounts, or lengthy loan processes. Of course, the use cases were very limited. Borrowers had to have collateral that they could deposit, and they couldn't take out more debt than they had collateral.

Why Use ETHLend?

The main use case for ETHLend was to allow people to unlock liquidity on their crypto assets. Unlocking liquidity means freeing up value that's trapped in assets that you can't sell so that you can spend it or use it to make other investments.

For example, let's say you were an early backer of the Uniswap project and own a lot of UNI tokens. You're convinced that UNI will continue to rise in price and don't want to sell the tokens. But perhaps you'd like to have some spending cash to make a big purchase - like the down payment on a new car. You could use ETHLend (or now, Aave) to free up some money to use on that down payment. You'd deposit UNI tokens to the platform, receive a loan in ETH, and then sell that ETH for USD. When it came time to pay back your loan, you would simply send back the loan principal and interest to the smart contract, freeing up your UNI tokens once again.

But ETHLend wasn't perfect. Because it used a peer to peer model to facilitate loans, users couldn't always take out loans on their assets. What if no one wanted to take the other side of your loan? There would be nothing to do but wait until someone was willing to lend you money.

What is Aave? How Does it Work Today?

In September 2018, ETHLend became Aave. (Fun fact: Aave is the Finnish word for ghost).

Aave's lending model differs from ETHLend's in that it is an on-demand loan platform. Users can deposit collateral and take out loans instantly without needing to find a lender and negotiate the terms of a loan.

Aave accomplishes this by making use of lending pools. Rather than matching lenders and borrowers for individual loans, Aave aggregates lenders into pools and allows borrowers to borrow assets from those pools. Terms are set up front based on the supply and demand of assets, allowing loans to be taken out instantly.

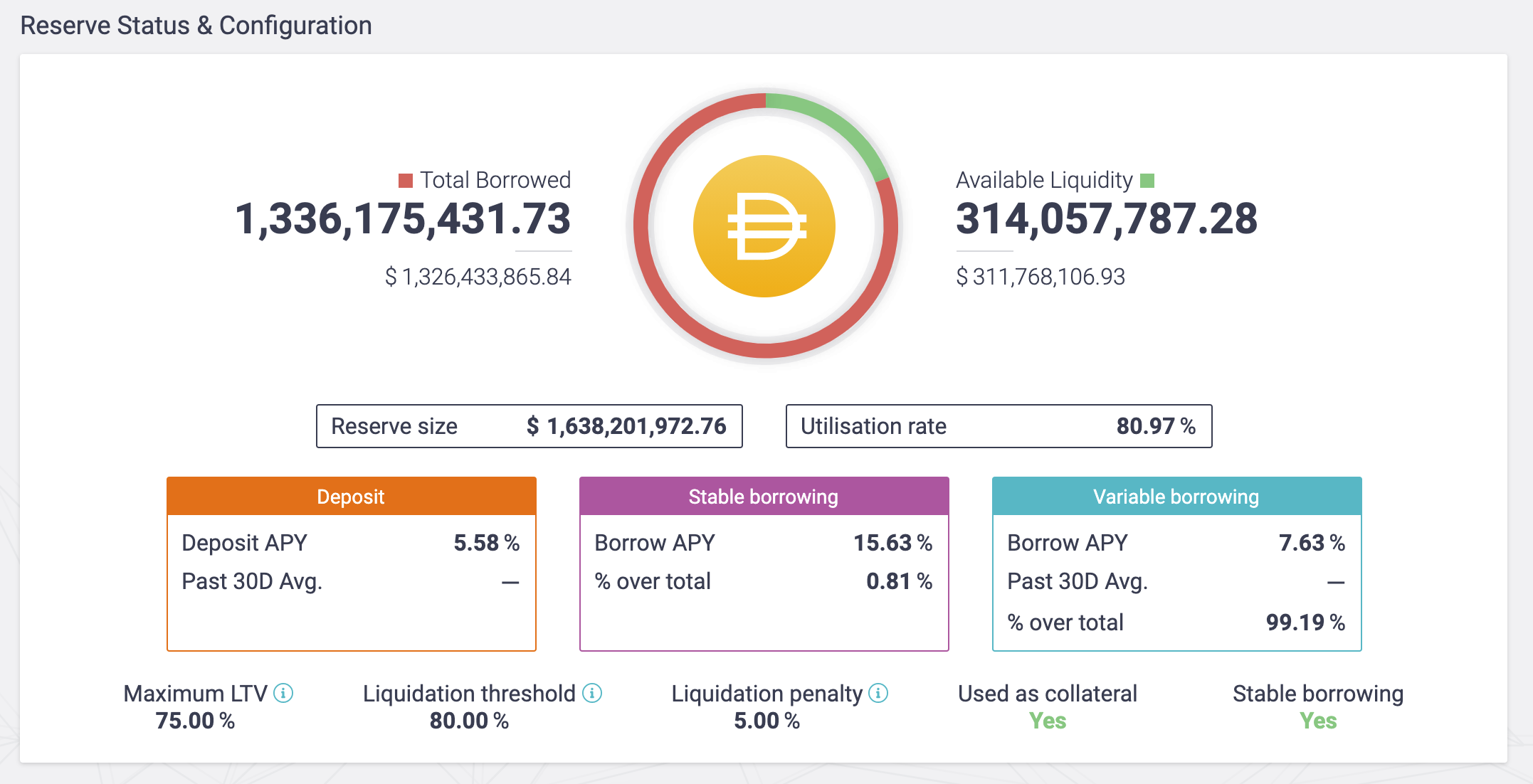

As you can see, interest earned on Aave from lending your assets is far higher than anything you'd be able to achieve at a bank (2.9-13.2% in the screenshot above).

Borrowing Assets on Aave

Let's take a look at the DAI lending pool. DAI is a popular stablecoin that is approximately equal to the US Dollar.

Every loan on Aave today is overcollateralized. That means that there is always more collateral posted than can be taken out in loans by borrowers. Aave must protect lenders by ensuring that they have enough capital to pay them back. In traditional finance, banks have other means of recovering bad loans. They can repossess a home or car or take the borrower to court. Because Aave's loans are anonymous, they don't have those options. Instead, they require loans to be overcollateralized. Providing undercollateralized loans is still a huge unsolved issue in crypto today. Several groups are working on it, but there hasn't been a widely adopted solution yet.

Two important risk metrics that Aave uses to mitigate the bad loan problem are the Loan to Value (LTV) figure and the liquidation threshold. The maximum LTV for the DAI contract is 75%. That means that when initiating a loan, you may take up to $75 in borrowed DAI for every $100 that you put up as collateral. This LTV parameter changes depending upon the asset. For example, the Ethereum lending pool has a maximum LTV of 80%.

The liquidation threshold is an important parameter to understand as well. Let's say that you took out a loan for $800 and put up $1,000 in ETH as collateral for that loan (taking out the maximum possible loan). If the price of ETH dropped, the amount of collateral that's covering your loan will also drop. If ETH falls far enough and your loan/ETH collateral is >82.5%, Aave will liquidate your ETH. You'll also be charged a 5% fee as a penalty for not maintaining enough collateral in the pool.

Rather than having fixed payback times, loans on Aave are indefinite; as long as you keep enough collateral on Aave, you can keep the loan alive.

Lending on Aave

When you deposit assets into a lending pool on Aave, you receive something called aTokens, or Aave interest-bearing tokens. For example, if you deposit 100 USDC to Aave, you'll receive 100 aUSDC to your wallet.

aTokens represent your claim on the lending pool. In other words, they represent the initial amount you deposited to the pool as well as your share of the interest earned by the pool. Because they represent the interest generated by the pool, you'll see the aToken balance in your wallet grow every second.

aTokens are simply ERC-20 tokens, meaning that you can sell them or transfer them to any other Ethereum wallet, thereby transferring your claim on the lending pool.

Implications for Traditional Finance

Aave follows the core principles of DeFi: it's open source, decentralized, and completely permissionless.

Because it's open source, anyone can fork the code and create a copy of it. Also, anyone can look at the code to audit it for security purposes.

Aave is also decentralized and permissionless. They cannot deny loans for users even if they wanted to! The protocol's code lives on Ethereum and has no gatekeepers. If you have the collateral for a loan, you can unlock liquidity on that collateral; you'll never be denied a loan based on race, gender, or ethnicity, as has happened and happens in traditional finance.

The use cases for Aave today are somewhat limited; users can only take out overcollateralized loans (not including flash loans, which is a special Aave product that's outside the scope of this article), and not everyone has crypto that they can use as collateral. Still, we are in the early days of DeFi. Ethereum and blockchain technology will allow us to come up with new ways of democratizing the loan market.

Traditional lenders should take note. While Aave isn't stealing much of their business today, as DeFi gains mass adoption, lending protocols like Aave and Compound will start to eat TradFi's lunch.

More on Aave

P.S. - I'm looking for feedback! Is there anything you found confusing? Are there any other topics in crypto you're keen to learn about?